The tsarma package implements methods for the estimation, inference, filtering, prediction and simulation of stationary time series using the ARMA(p,q)-X model. It makes use of the tsmodels framework, providing common methods with similar inputs and classes with similar outputs.

The Appendix provides a table with a hierarchical overview of the main functions and methods currently implemented in the package.

2 Estimation

The ARMA(p,q)-X model implemented in the package has the following representation:

where \(x\) is an optional matrix of external pre-lagged regressors with coefficients \(\xi\). The ARMA coefficients are \(\phi\) and \(\theta\) respectively, constrained during estimation so that their inverse roots are less than unity. The residuals \(\varepsilon_t\) can be modeled using one of the distributions implemented in the tsdistributions package with additional parameters (\(\ldots\)) to capture higher order moments. Both \(\mu\) and \(\sigma\) are estimated, not concentrated out.

Initialization of the ARMA recursion proceeds as follows:

For a ARMA(p,q) or ARMA (p,0) model with \(p > 0\), the recursion is initialized at time \(t=p+1\) so that p degrees of freedom are used up. If an MA term is present (\(q>0\)), then it will also be initialized at time \(t=p+1\) irrespective of the MA order, allowing all terms in the MA component (\(j=\left(1,\ldots,q\right)\)) for which \(t>j\) to contribute to the initial fitted values.

For an ARMA(0,q) model with \(q>0\), the recursion is initialized at time \(t=2\) allowing all terms in the MA component (\(j=\left(1,\ldots,q\right)\)) for which \(t>j\) to contribute to the initial fitted values.

Initial values for the coefficients proceed by first trying a pass through the stats::arima function, and if that fails, then then the method of Hannan and Rissanen (1982) is used instead.

Estimation uses the nloptr solver with analytic gradients provided through the use of the TMB package for which a custom C++ functions have been created written to minimize the log-likelihood subject to the distribution chosen. Inequality constraints for stationarity (AR) and invertibility (MA) are imposed and their Jacobians calculated using jacobian function from the the numDeriv package.

Standard errors are implemented with methods for bread and estfun (scores), in addition to functions for meat and meat_HAC using the sandwich package framework.

3 Demonstration

3.1 Estimation

We demonstrate the functionality of the package using the SPY ETF price series from the tsdatasets package using an ARMA(2,1) model, after taking log differences.

Code

spy <- tsdatasets::spyspyr <-diff(log(spy$Close))[-1]spec <-arma_modelspec(spyr[1:2000], order =c(2,1), distribution ="jsu")mod <-estimate(spec)summary(mod, vcov_type ="QMLE")

The summary method has an optional argument for the type of coefficient covariance matrix to use for calculating the standard errors. Valid options are the analytic hessian (“H”), outer product of gradients (“OP”), Quasi-MLE (“QMLE”) and Newey-West (“NW”) for which additional arguments can be passed (see the bwNeweyWest function in the sandwich package).

A nicer table can be generated using the as_flextable method, which we illustrate below:

There are options to control what goes into the table and whether parameters should be kept with their names or symbols. The model equation is generated from the tsequation method.

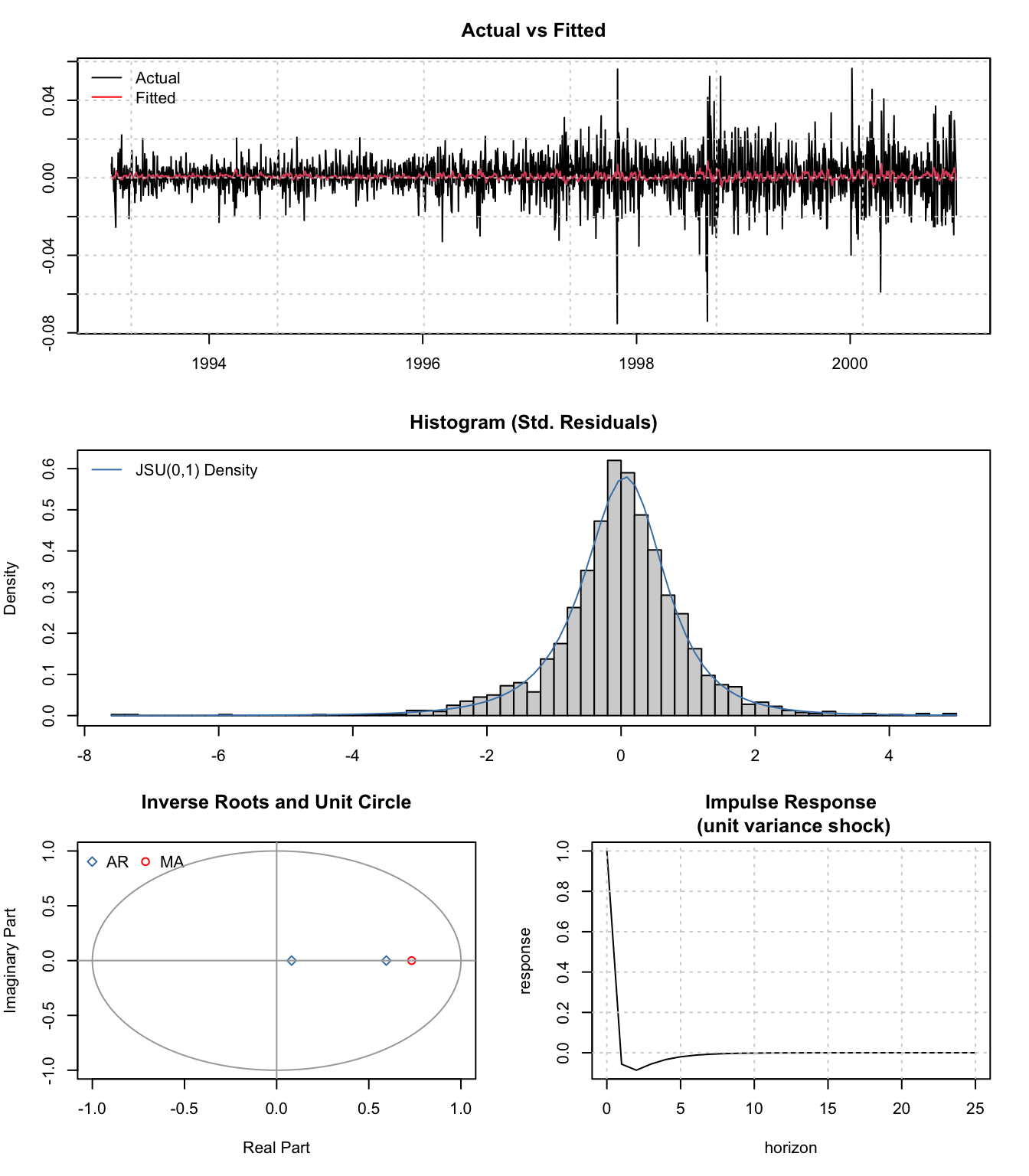

The plot method on the estimated object generates a set of 4 plots of the fitted against actual values, the histogram of the standardized residuals against the expected density of the distribution used, and the ARMA inverse roots and impulse response function.

Code

plot(mod)

The impulse response function (arma_irf) of this model shows that a unit variance shock will decay to zero after about 5 periods.

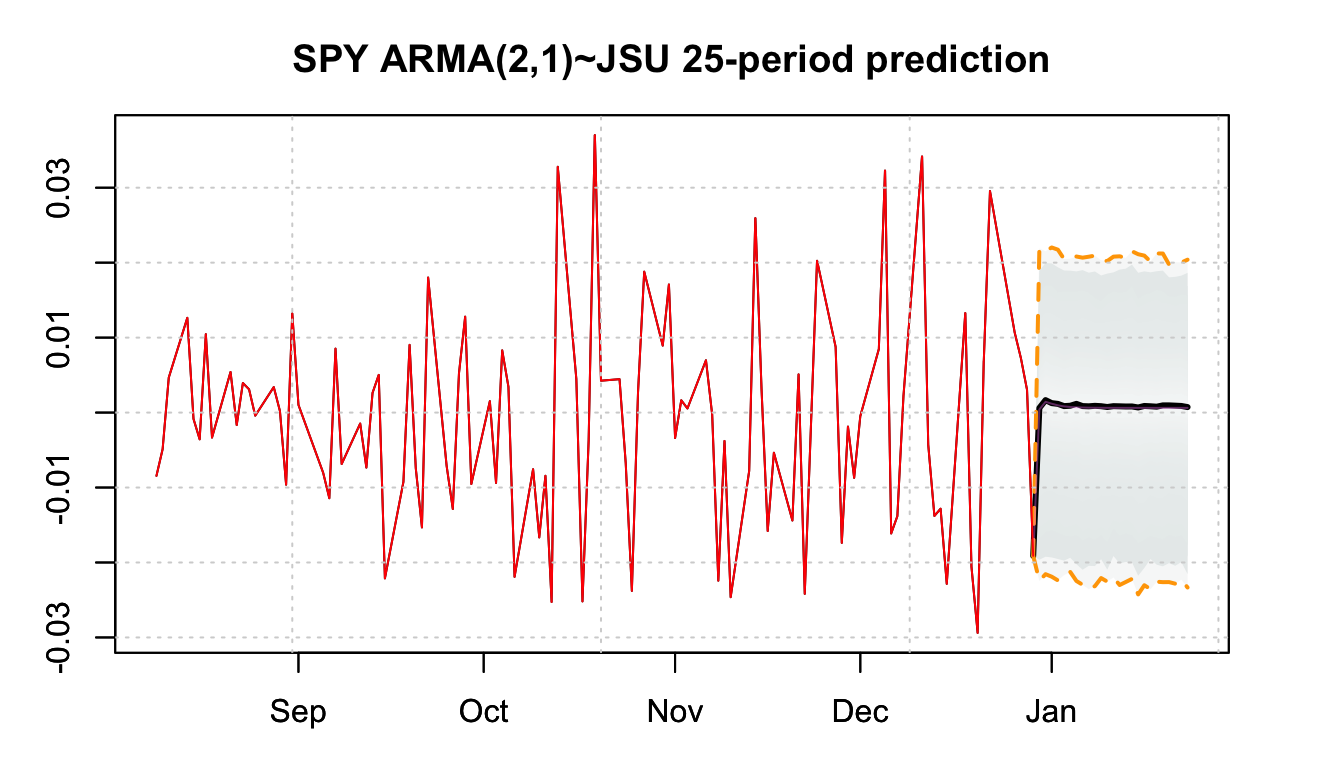

3.2 Prediction

The predict method will generate h step ahead predictions of the conditional mean, the model standard deviation as well as a simulated predictive distribution using either bootstrap re-sampling of the residuals else parametric sampling based on the distribution chosen to estimate the model. Optionally, the user can pass in a matrix of innovations to be used instead. These can either be uniform deviates (in effect quantiles) which will be transformed into the model’s distributional innovations, standardized innovations which will be scaled by the standard deviation of the model, else non-standardized innovations. The latter may be useful when passing a GARCH generated set of forecast innovations.

The forc_dates argument allows the user to pass a set of time indices representing the forecast horizon, else the function will try to auto-generate these based on the estimated sampling frequency of the data.

Code

p <-predict(mod, h =25, bootstrap =TRUE, nsim =5000)head(cbind(p$mean, p$sigma))

The variance of the prediction error at time \(t+h\) is equal to:

\[

\hat \sigma\sum^{h-1}_{i=0}\Psi^2_i

\tag{3}\]

where \(\Psi\) represent the infinite MA representation of an ARMA(p,q) model (psi-weights), which can be generated using the stats::ARMAtoMA function.

Since the output is of class tsmodel.predict, the corresponding plot method from the tsmethods package can be used directly.

The 2 final methods of note in the package are tsfilter and simulate which allow the filtering of new data and simulation, respectively. Both of these methods can be dispatched from either an estimated model of class tsarma.estimate as well as a specification object of class tsarma.spec. In the following demonstration, the combination of tsfilter and simulate methods is illustrated.

We first take the original specification object and replace the parameter matrix holding the estimated parameters from the estimated object. This is all that is required.

In the next step we verify that tsfilter both the specification and estimated objects return the same result.

Code

filter_spec <-tsfilter(spec, y = spyr[2001:2010])filter_model <-tsfilter(mod, y = spyr[2001:2010])all.equal(fitted(filter_spec), fitted(filter_model))

[1] TRUE

Filtering on a specification object is equivalent to running through the ARMA recursion with fixed parameters. We can check that passing a specification object without new data to tsfilter will results in the same values as those from the estimated model.

It is also possible to completely replace y with a new dataset if we have pooled estimates of the parameters to use in the parameter matrix. Simply put, the filtering algorithm takes a set of fixed parameters and filters the data.

Next, we illustrate how to generate a predictive distribution using the simulate method on both the estimated and specification objects and verify replication of results with the predict method.

Code

sim_spec <- specsim_spec$parmatrix <-copy(mod$parmatrix)filter_spec <-tsfilter(sim_spec)maxpq <-max(spec$model$order)series_init <-tail(sim_spec$target$y_orig, maxpq)innov_init <-as.numeric(tail(residuals(filter_spec), maxpq))simulate_spec <-simulate(sim_spec, nsim =2000, seed =100, h =10, series_init = series_init, innov_init = innov_init)simulate_model <-simulate(mod, nsim =2000, seed =100, h =10, series_init = series_init, innov_init = innov_init)set.seed(100)p <-predict(mod, h =10, nsim =2000)# equivalence between estimation and specification simulated distributionsall.equal(simulate_spec$simulated, simulate_model$simulated)

[1] TRUE

Code

# equivalence between simulation method and prediction method distributionsall.equal(simulate_spec$simulated, p$distribution)

[1] TRUE

4 Conclusion

The tsarma package is currently under development and may change in the future. Potential areas for improvement are likely to be the inclusion of non-stationary series turning it into an ARIMA model. Adding seasonality is not something which is planned, and users who work with stationary seasonal series can use fourier terms in the regressors using the fourier_series function from tsaux.

5 Appendix

5.1 Methods and Classes

(...)

type

input

output

tsarma

¦--arma_modelspec

function

xts

tsarma.spec

¦¦--simulate

method

tsarma.spec

tsarma.simulate

¦¦--tsfilter

method

tsarma.spec

tsarma.estimate

¦°--tsbacktest

method

tsarma.spec

list

¦--estimate

method

tsarma.spec

tsarma.estimate

¦¦--summary

method

tsarma.estimate

summary.tsarma

¦¦°--print

method

summary.tsarma

print/flextable

¦¦--tidy

method

tsarma.estimate

tibble

¦¦--glance

method

tsarma.estimate

tibble

¦¦--plot

method

tsarma.estimate

plot

¦¦--coef

method

tsarma.estimate

numeric

¦¦--logLik

method

tsarma.estimate

logLik

¦¦--fitted

method

tsarma.estimate

xts

¦¦--residuals

method

tsarma.estimate

xts

¦¦--tsequation

method

tsarma.estimate

list

¦¦--AIC

method

tsarma.estimate

numeric

¦¦--BIC

method

tsarma.estimate

numeric

¦¦--confint

method

tsarma.estimate

matrix

¦¦--vcov

method

tsarma.estimate

matrix

¦¦--bread

method

tsarma.estimate

matrix

¦¦--estfun

method

tsarma.estimate

matrix

¦¦--predict

method

tsarma.estimate

tsmodel.predict

¦¦¦--plot

method

tsmodel.predict

plot

¦¦°--pit

method

tsarma.predict

xts

¦¦--simulate

method

tsarma.estimate

tsmodel.simulate

¦¦--tsfilter

method

tsarma.estimate

tsmodel.estimate

¦¦--unconditional

method

tsarma.estimate

numeric

¦¦--sigma

method

tsarma.estimate

numeric

¦¦--nobs

method

tsarma.estimate

numeric

¦¦--pit

method

tsarma.estimate

xts

¦°--halflife

method

numeric

numeric

¦--arma_irf

function

numeric

arma.irf

¦°--plot

method

arma.irf

plot

°--arma_roots

function

numeric

arma.roots

°--plot

method

arma.roots

plot

6 References

Hannan, Edward J, and Jorma Rissanen, 1982, Recursive estimation of mixed autoregressive-moving average order, Biometrika 69, 81–94.